Trading EdgeTest the Rule Before You Trade It

A trading signal is only useful after it survives the parts most backtests avoid.

We test technical rules against data-snooping, transaction costs, taxes, and out-of-sample evidence.

Backtest Evidence

Trading Costs

Out-of-Sample Tests

The Survival Test

How We Test a Claimed Trading Edge

A profitable chart in hindsight is not enough. The analysis has to show that the rule was defined before the result, survives realistic execution costs, and continues to work outside the sample that produced it.

01 · Signal

Was the rule defined clearly?

We separate testable entry and exit rules from visual pattern recognition that changes after the chart is already known.

02 · Friction

Does the edge survive implementation?

Turnover, spreads, slippage, taxes, and missed market exposure are included before a gross backtest is called investable.

03 · Survival

Does it work beyond the original sample?

We look for multiple-testing corrections, regime robustness, and out-of-sample evidence rather than rewarding one attractive historical period.

Backtest analysis for education and further research, not a recommendation to trade any signal or security.

Research Library

Latest Trading Edge Analysis

Technical signals, backtest failures, execution costs, market timing rules, and evidence that survives hindsight.

Jun 1, 2026

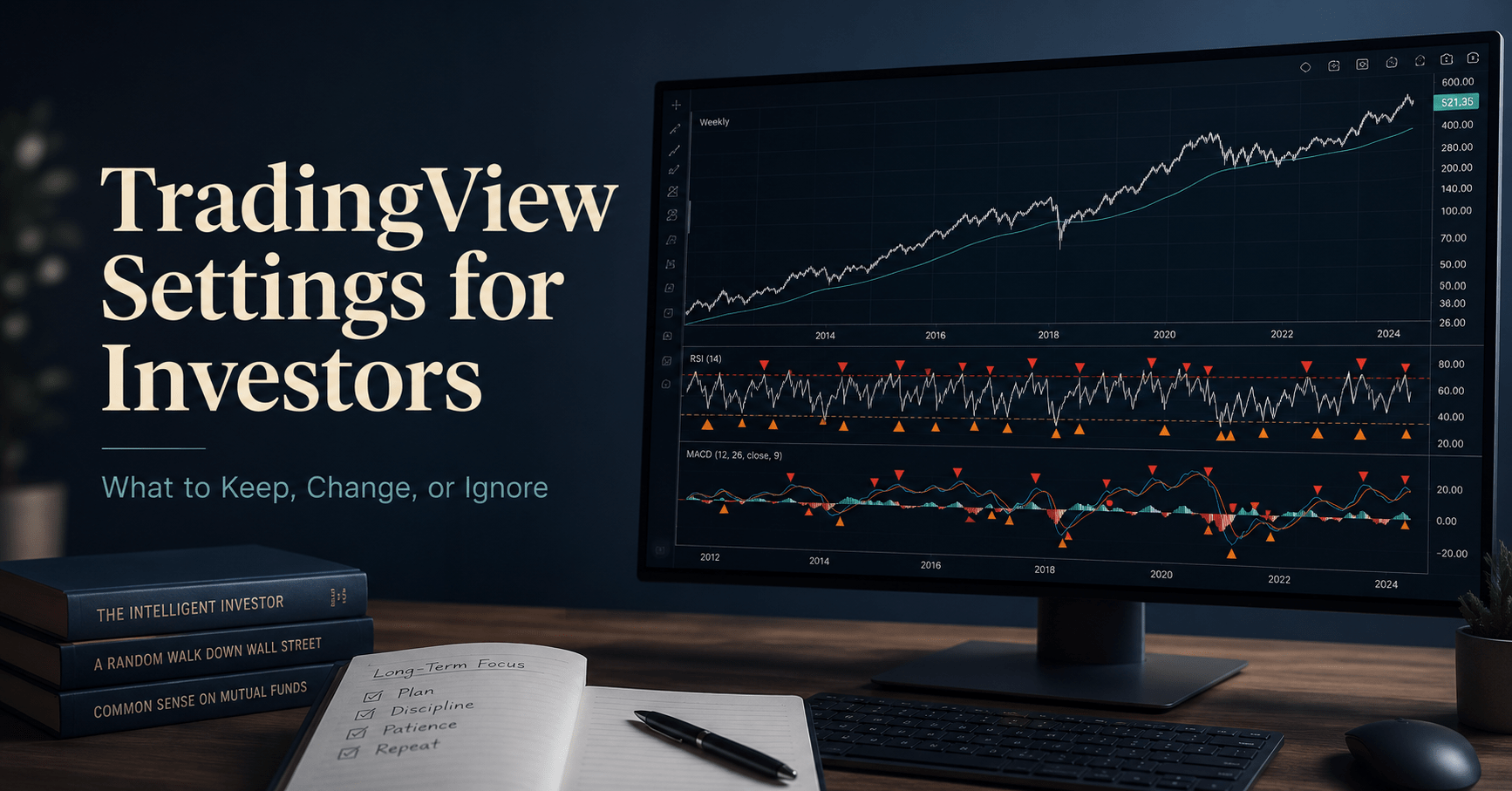

TradingView Settings for Investors: What to Keep, Change, or Ignore

TradingView's default RSI 14 and MACD 12/26/9 are 1970s day-trading numbers. Obey their alerts as a long-term investor and the quiet bill runs about $4,757 a decade.

Read the analysis →

May 25, 2026

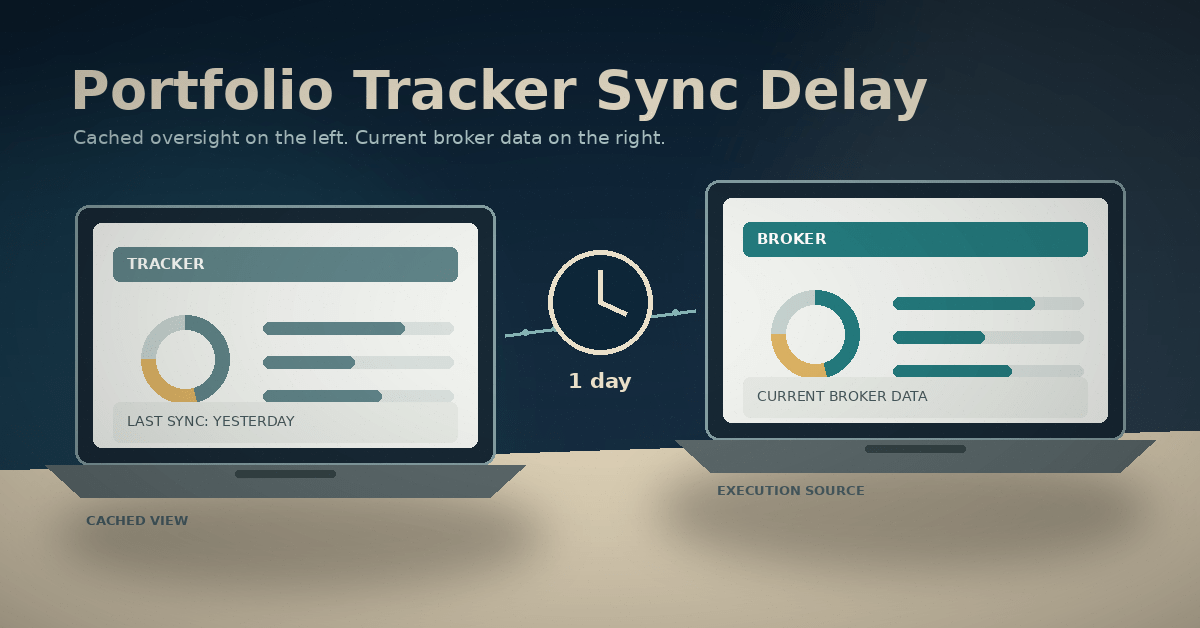

Portfolio Tracker Sync Delay: When Fresh Data Actually Matters

We ran 3,000 simulations to price a day-late portfolio tracker. Median 30-year cost: about zero. It adds swing, not a steady drain.

Read the analysis →

May 22, 2026

Does Volume Precede Price? What the Research Actually Shows

📅 Originally Published: May 21, 2026 · Last Updated: July 23, 2026 Trading volume can add context, but the research reviewed here does not support a universal rule that it…

Read the analysis →

May 19, 2026

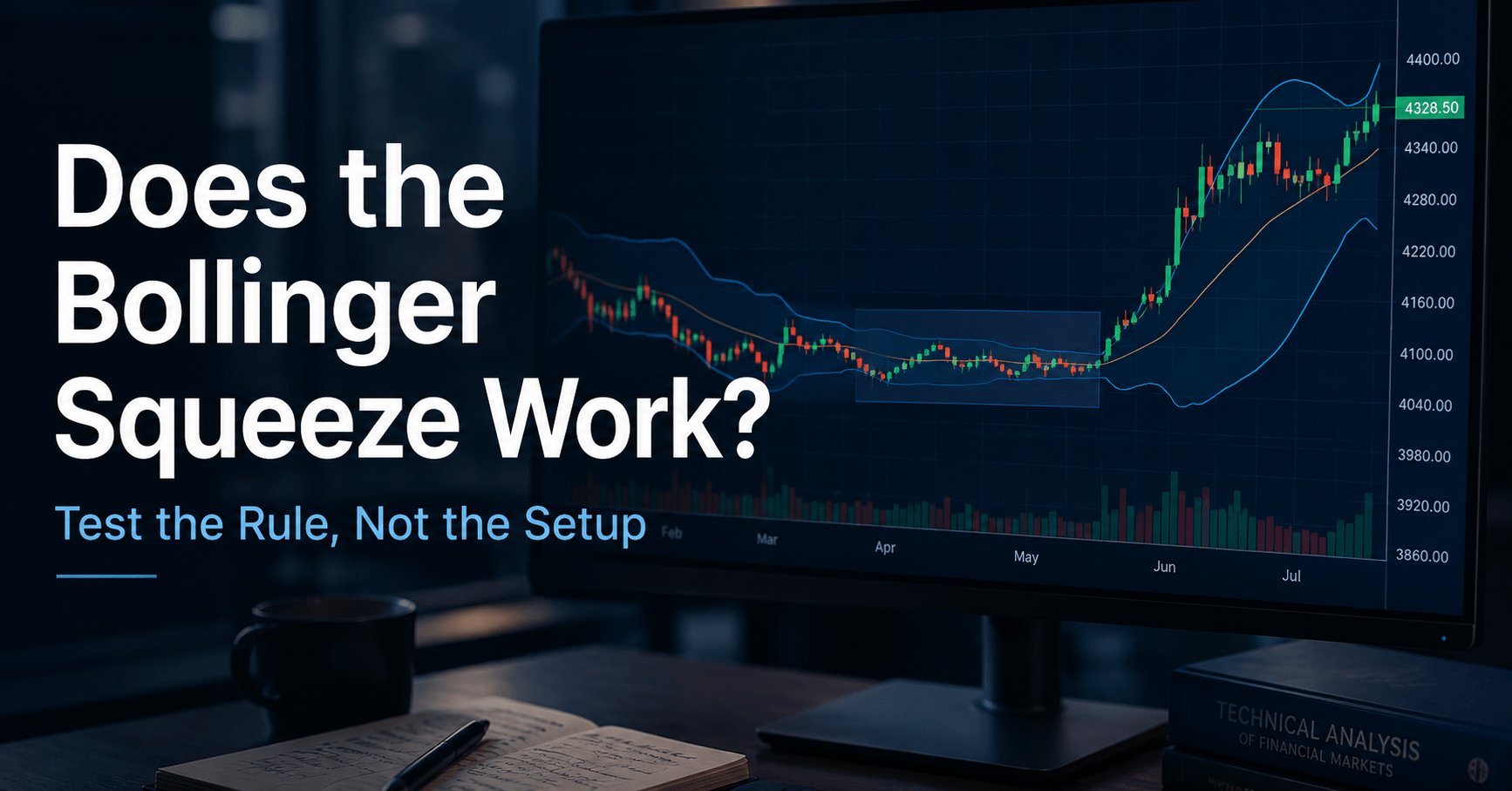

Does the Bollinger Squeeze Work? Test the Rule, Not the Setup

Bollinger Band squeeze win rate sits at 50 percent in academic tests of 7,846 trading rules. The compound cost on a $50,000 account over 15 years reaches $26,328.

Read the analysis →

May 16, 2026

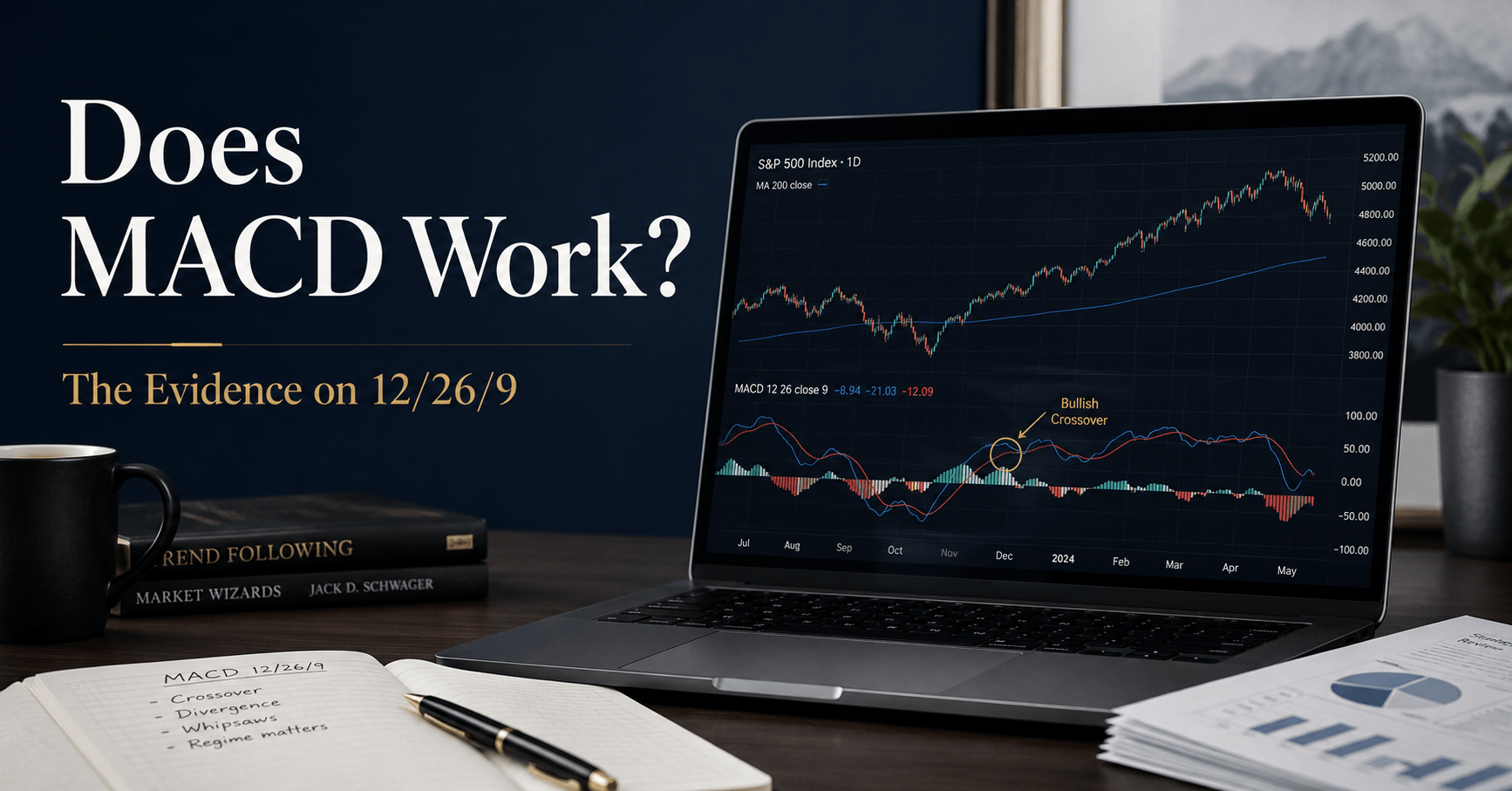

Does MACD Work? What the Evidence Says About 12/26/9

The common 12/26/9 MACD setting is easy to add to a chart, but the evidence does not support treating it as a universal trading edge.

Read the analysis →

May 13, 2026

RSI Overbought Signal: Why 70 Is Not an Automatic Sell

An RSI overbought signal above 70 shows unusually strong recent momentum. It does not, by itself, tell you to sell

Read the analysis →

May 11, 2026

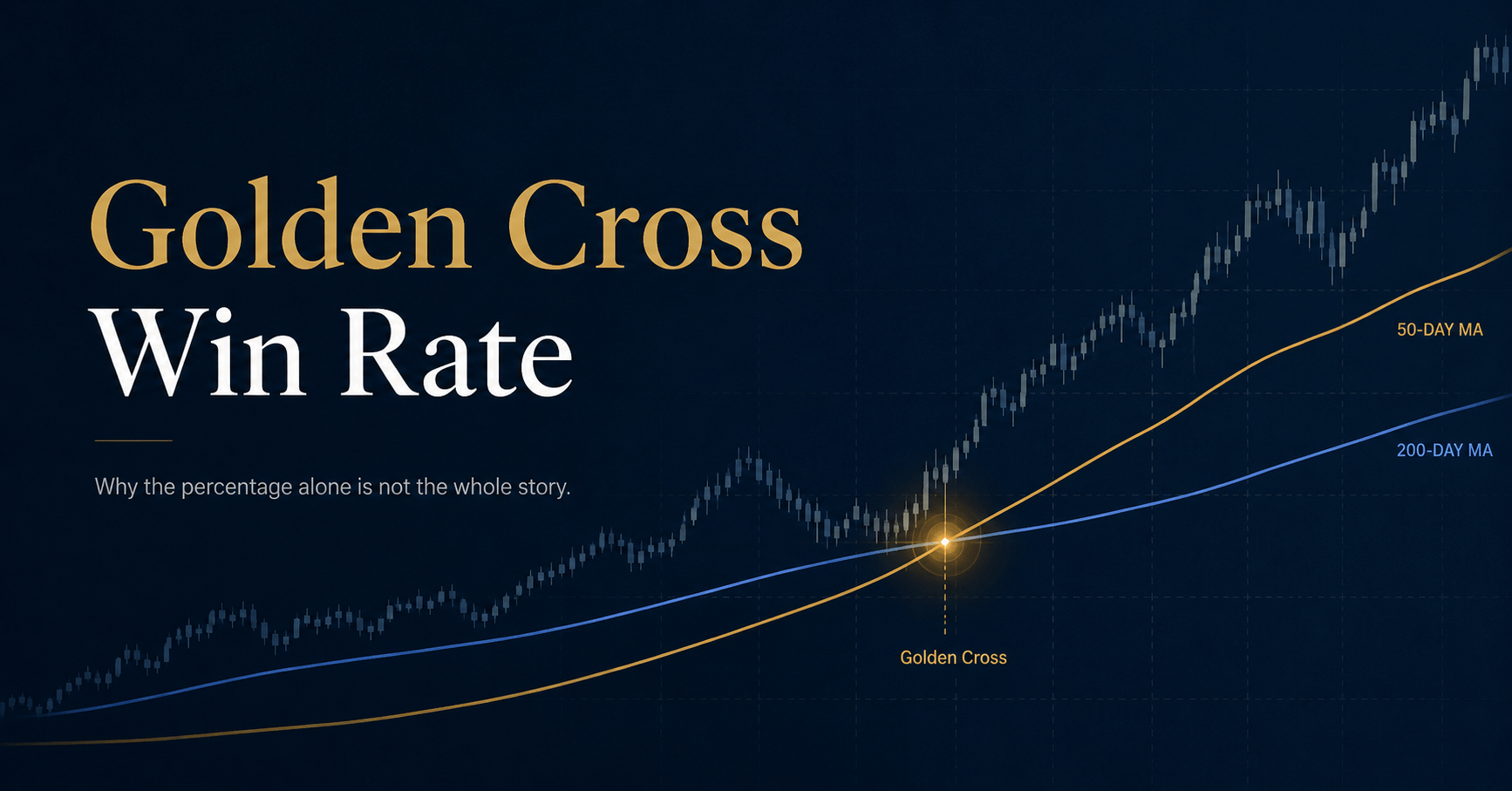

Golden Cross Win Rate: What the Percentage Misses

A 78 percent golden cross win rate is a frequency claim, not a wealth claim. QuantifiedStrategies' 33-signal S&P 500 backtest from 1960 through 2026 logs the 78 percent figure alongside…

Read the analysis →

May 8, 2026

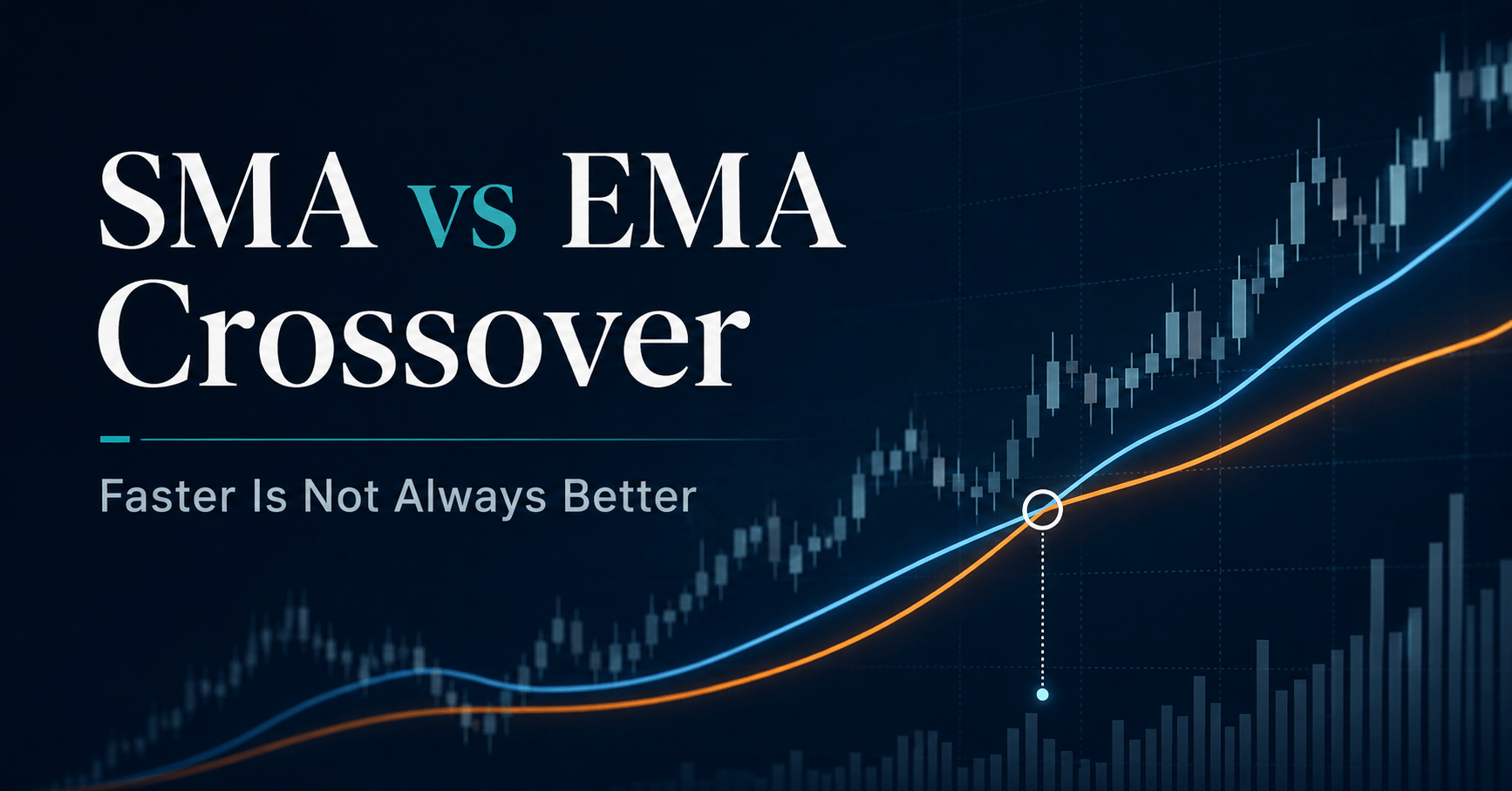

SMA vs EMA Crossover: Faster Is Not Always Better

Barber and Odean's Q4 turnover quintile costs 5.568 percent yearly across 66,465 households. That drag attaches to trade frequency, not signal smoothness.

Read the analysis →

May 6, 2026

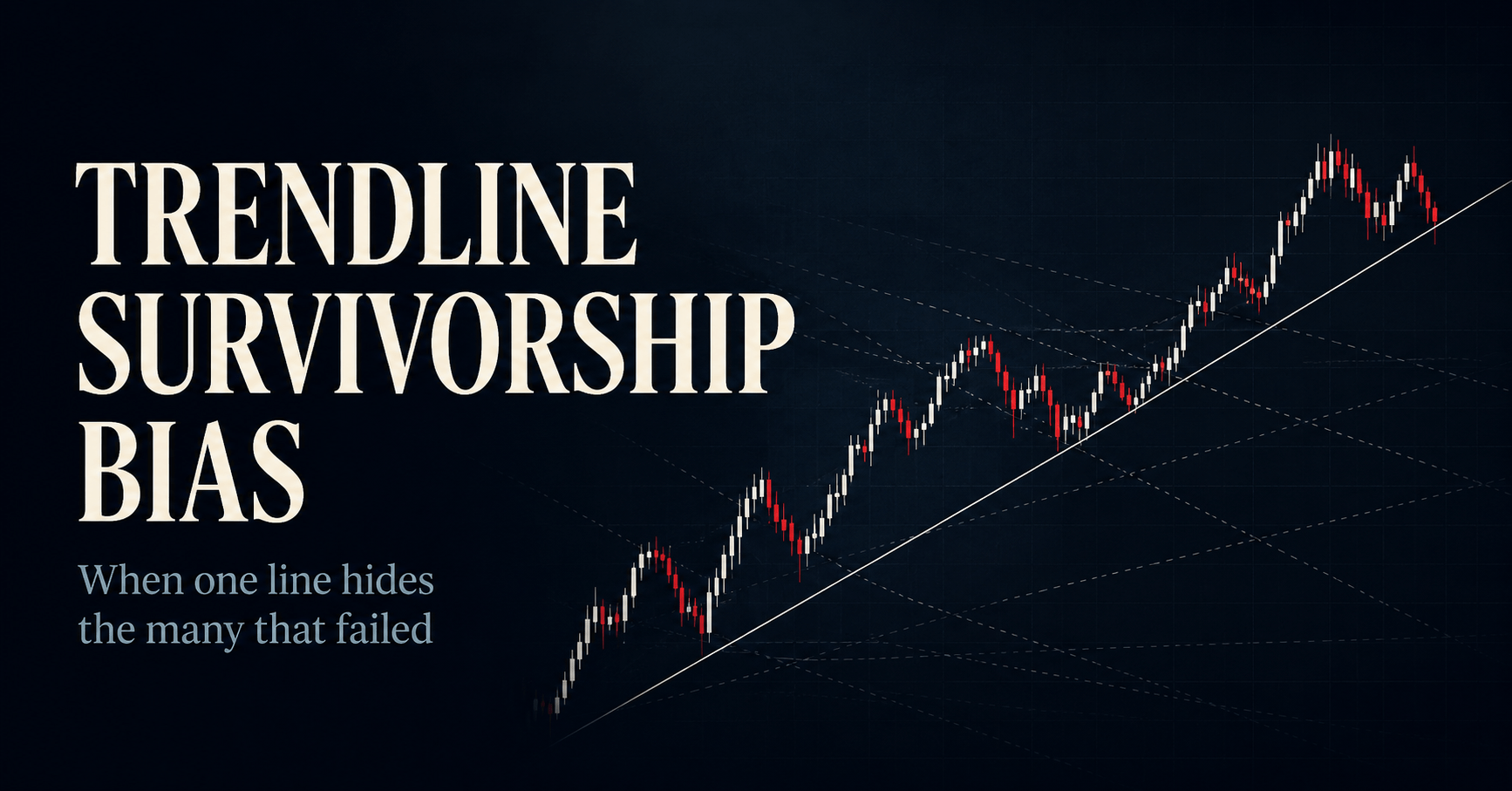

Trendline Survivorship Bias: Why a Line That Worked Can Mislead You

Retail trendline trading looks free but compounds 1% drag into a $598,099 wealth gap on $200K over 35 years. The chart never shows what it deleted.

Read the analysis →

May 4, 2026

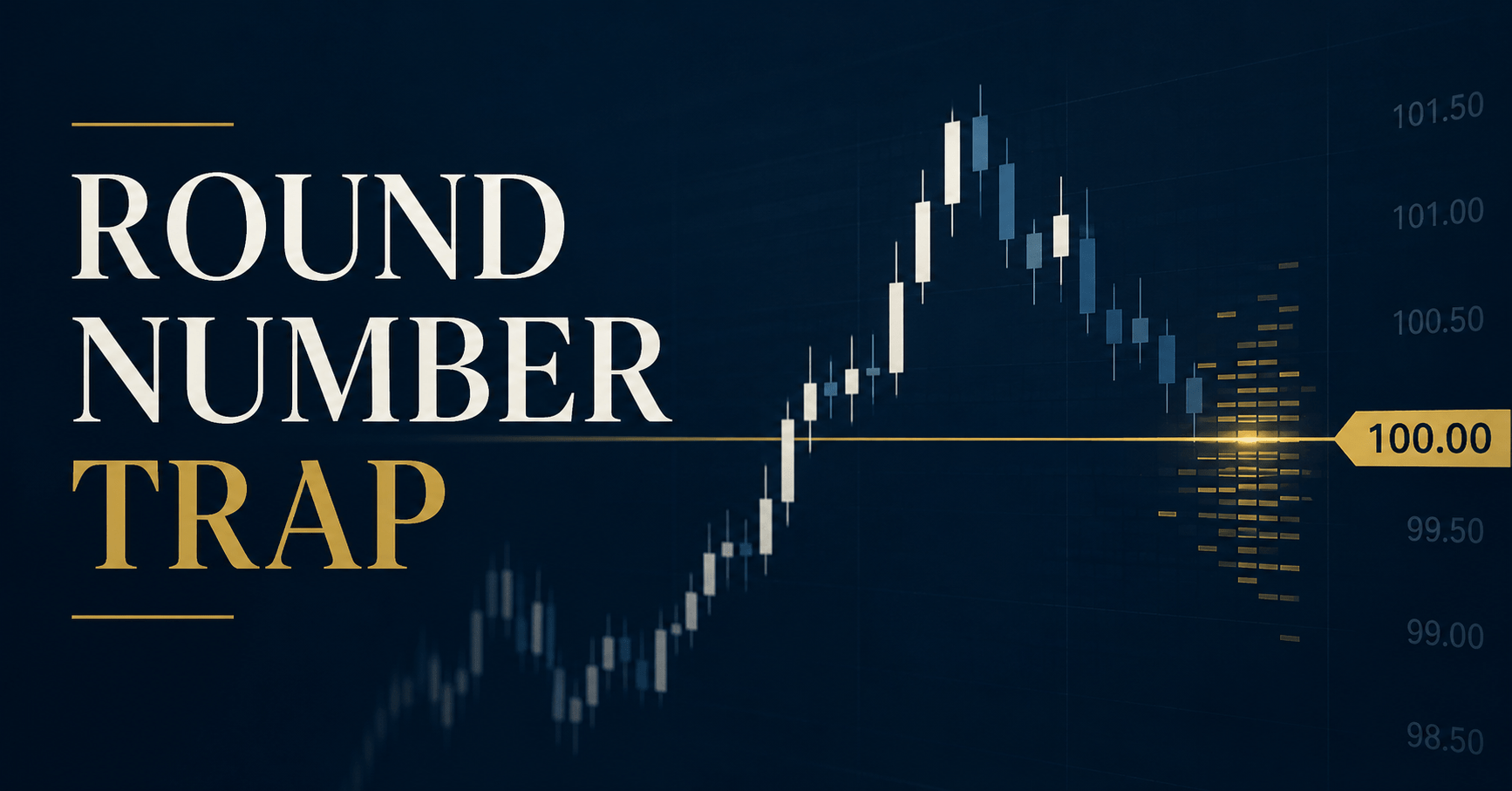

Support and Resistance at Round Numbers: What the Data Actually Shows

Round prices attract measurable trading attention, but the evidence does not show that they reliably hold or reverse. This guide separates clustering from prediction and gives a practical order-decision framework.

Read the analysis →